630-409-8184

630-409-8184What Happens if the House Goes into Foreclosure During Divorce?

Foreclosures are on the rise in Illinois, ranking the state as the ninth highest for home foreclosures. This translates to one out of every 3,753 homeowners facing foreclosure of their homes. This unfortunate trend shows little signs of slowing or reversing.

Foreclosures are on the rise in Illinois, ranking the state as the ninth highest for home foreclosures. This translates to one out of every 3,753 homeowners facing foreclosure of their homes. This unfortunate trend shows little signs of slowing or reversing.

Foreclosure by itself is a difficult process for a couple to weather. A couple who is in the middle of a divorce when served with a foreclosure notification can see the difficulties compound rapidly, especially when both spouses are not on the same page regarding how to deal with the foreclosure.

There is much information to disseminate and several options to discuss. If you and your spouse are divorcing and are now facing the foreclosure of your marital home, it can be extremely beneficial to discuss the situation with an experienced Oswego, IL divorce lawyer.

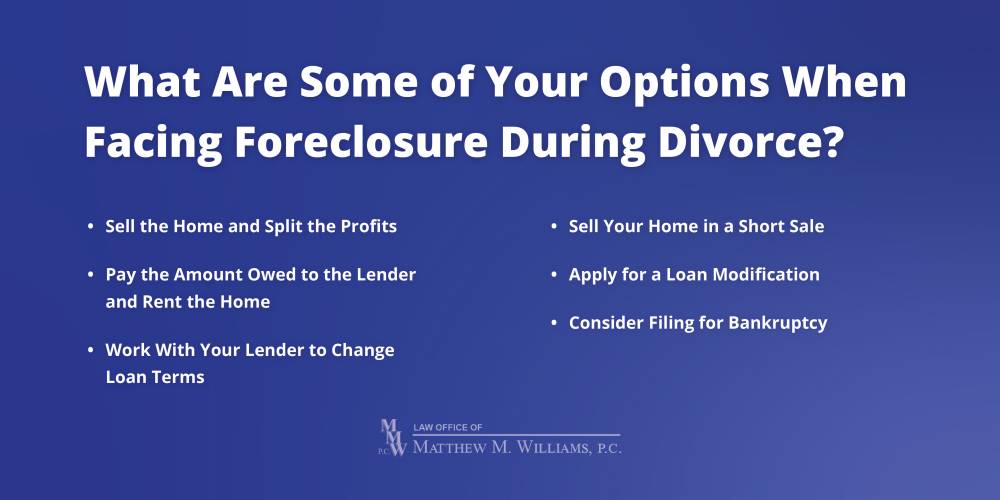

What Are Some of Your Options When Facing Foreclosure During Divorce?

The options you will face when filing for divorce and dealing with foreclosure will depend largely on whether you have significant equity in your home or are underwater with your mortgage (you owe more than it is worth). Divorce, on its own, cannot stop foreclosure. If your house is in pre-foreclosure or the beginning of foreclosure, there may be options that both of you can agree on. If you have equity in your home, you may have the following options:

Sell the Home and Split the Profits

You can sell your home when it is in pre-foreclosure or foreclosure. You will have to pay the lender what is owed to stop the foreclosure by borrowing the money or selling another asset. You can then put the home up for sale, and once it sells, you can split the profits between you and your spouse during the division of marital assets portion of your divorce.

One Spouse Wants to Keep the Home

If you or your spouse wants to keep the marital home, then that spouse will also be responsible for the monthly mortgage payments. The amount of equity in the home will determine how the remainder of the marital assets are split; once that amount is determined, the spouse who does not want to keep the house will be awarded assets equal to the home's equity.

At this point, the spouse who wants to keep the home should know how he or she plans to prevent foreclosure. That spouse will assume the loan, releasing the other spouse from the mortgage obligation. Once that is accomplished, the spouse keeping the home could get a loan modification, catch up on the payments, and refinance the home only in his or her name.

Pay the Amount Owed to the Lender and Rent the Home

Rentals are booming right now, so if you or your spouse do not want to sell the home, another option is to pay your lender what you owe, stop the foreclosure, and then rent the house out for more than the monthly mortgage. Keep in mind that the person responsible for renting the house may have to deal with bad renters and constant repairs, so this might only be worth it if you can rent the house for significantly more than the mortgage. There may also be tax issues associated with renting out your home.

If You Are Underwater on Your Mortgage

If you and your spouse owe more than your house is worth, your options become more limited and more difficult. Some of the solutions to consider include:

Work With Your Lender to Change Loan Terms

If your lender is willing, you and your spouse can work with the mortgage holder to lower the monthly payments and perhaps place the past-due mortgage payments on the back end of the mortgage. Lenders are not often willing to do this when a couple is divorcing because the likelihood that they will get their money goes down when only one spouse is responsible for the payments.

Sell Your Home in a Short Sale

If you owe more than your home is worth, you might consider a short sale: selling your home to a buyer for less than the amount you owe on your mortgage. The potential benefit here is that your lender might agree not to go after you for the deficiency (the difference). For example, your house is worth $400,000, and your loan balance is $425,000. You sell the house for $400,000, and your lender agrees to take a $25,000 loss. You and your spouse walk away with no debt but no house.

Do Not Fight the Foreclosure

You and your spouse may agree to let the foreclosure happen. The home will not be considered an asset when dividing up the marital assets, but it will damage both your and your spouse’s credit score for several years, making it difficult for you to rent a home or buy another home.

Apply for a Loan Modification

If you or your spouse wants to keep the home even though you are underwater with your mortgage, the house could be awarded to one of you in the divorce, then that person could ask the lender to lower the interest rate and extend the terms of the loan to reduce the monthly payment amounts. It is generally better to wait until the divorce is final to do this, so that both spouses are not responsible for the modification of the mortgage, but the person awarded the home should make sure he or she qualifies for the loan modification.

Consider Filing for Bankruptcy

If your mortgage is not the only past-due debt you and your spouse have, and you are struggling to pay your monthly bills, you can potentially eliminate or reduce your debt load while keeping your home by filing for bankruptcy. Filing Chapter 7 bankruptcy jointly will discharge the debts of both spouses, giving you both a fresh financial start after the divorce. Plus, it is less expensive to file for bankruptcy together than individually. If you are planning to file for Chapter 13 bankruptcy, you should do so after the divorce is final, on your own, since there is a three-to-five-year payment plan.

Contact a Kendall County, IL Divorce Lawyer

Although foreclosure proceedings during a divorce can complicate matters, it does not have to derail your life completely. Speaking to a Yorkville, IL divorce lawyer from The Law Office of Matthew M. Williams, P.C. can significantly affect the outcome of your divorce and your foreclosure. Attorney Williams focuses his practice on mediation and collaborative divorce to make the process easier and less expensive for both parties. Call 630-409-8184 to schedule an initial attorney meeting.

Ready to Get Started?

To schedule a free consultation with Aurora divorce attorney, Matthew M. Williams, call 630-409-8184 or fill out the form below.

Aurora

1444 North Farnsworth Ave., #307

Aurora, IL 60505

P 630-409-8184

MAP + DIRECTIONS

BY APPOINTMENT ONLY

Yorkville

215 Hillcrest Ave., Suite A5

Yorkville, IL 60560

P 630-409-8184

MAP + DIRECTIONS